This month we are privileged to have a guest writer: Andrew Postell, VP of Mortgage Lending at Guaranteed Rate.

Tax season is fast approaching and that means many of us will need to file our Federal Tax Returns. Even if you are filing an extension I have tried to put some things together here that will help you DECREASE your personal tax liability and INCREASE your income for qualifying for a Fannie Mae and Freddie Mac type of loan.

This post is designed to help persons who may need a Fannie/Freddie loan on a 1-4 unit property. There are lots of reasons why this might be you…but alternatively there are MANY an investor that are very successful WITHOUT Fannie Mae or Freddie Mac. But if you would like to take advantage of their rates and terms while at the same time decreasing your tax burden then this post is for you!

Here’s what I mean:

When you file your tax returns there are certain deductions that can be added BACK to your income to help you qualify for a Fannie/Freddie type of loan. Keep in mind if you are doing commercial/portfolio/other loan types then none of this may matter…but for Fannie/Freddie it will.

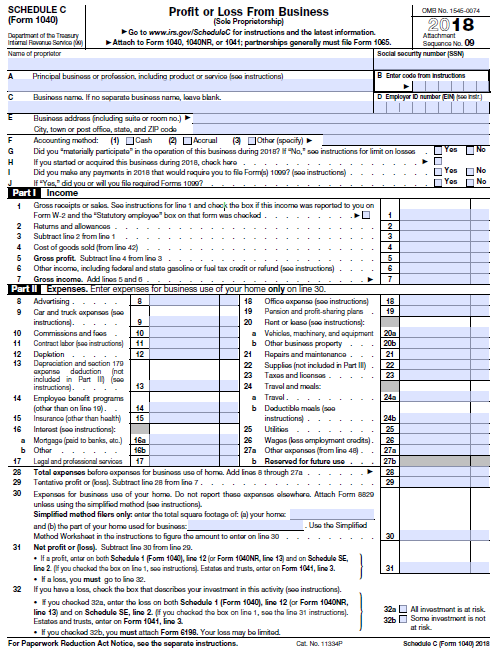

SCHEDULE C

The Schedule C portion of your personal tax returns is where most people file an active business that is operated as a “sole proprietorship.” Basically any business that is not a Partnership, S-Corp, C-Corp. Even a single-member LLC can be claimed here as well.

I have included an image of the page below and you can see the basic layout: Income and Expenses mostly. So the income is claimed at the top and the expenses are DEDUCTED toward the bottom. These deductions are what we want to focus on.

Deductions help REDUCE your taxable income. So if you made $100 (on line 1) but used $100 in advertising (line 8) your taxable income (line 31) would be $0. Now, this is just for an example….hopefully no one is actually doing this as you would make $0 as a company. This is however one of the main reasons self-employed persons report having issues with banks – NOT ENOUGH TAXABLE INCOME. What are you to do if you want to write everything off but still look good towards a lender? Here’s your answer:

- Depreciation (Line 13/14) – can be added BACK as income

- Business Use of Home (Line 30) – can be added BACK as income

- Vehicle Miles (Line 44A) – can be added BACK as income

- Un-allowed Meals and Entertainment (Line 24B) – is subtracted FROM your income

If you have a choice on HOW to deduct the items above then you want to CHOOSE to try to deduct them in those categories. What I mean here is that many people deduct their automobile expense in Line 9 – Car and Truck Expenses…..and you might be correct that itemizing your automobile deductions might allow you to get a HIGHER deduction when using this line….but your lender cannot add it back to your income! However, Line 44A – Can absolutely be added back to your income! So if you have a choice of deducting in Line 9 or Line 44A…then choose LINE 44A for Fannie Mae!

Likewise, if you are working out of your home then you should be fully realizing Line 30. This will help reduce your taxes but get added back to your income (again, for Fannie/Freddie loans).

Let’s use an example:

Let’s say your company earned $10,000. But you wrote off $5,000 in Depreciation (Line 13/14). $2,500 in Use of Home (Line 30). And claimed $2,500 in mileage (Line 44A)…then your TAXABLE INCOME (Line 31) would be ZERO! Oh no! But wait…..your lender gets to add those 3 items back as income. So your taxable income is still ZERO but your qualifying income is $10,000! Now imagine if this was $20,000….or $50,000…and on an on! I hope you see where we are going with this. And this is just ONE Schedule. Ready for another?

SCHEDULE E

Schedule E is where we show our properties and get to write off everything! Cleaning, Insurance, Maintenance, Taxes, and on and on and on.

And Schedule E has some very similar themes to it as well….some deductions can be added BACK to your qualifying income while at the same time REDUCING your taxable liability. Here’s what you should know on Schedule E:

- Depreciation (Line 18) – can be added BACK

- Casualty Loss/Amortization/One-Time Expenses/HOA Dues (line 19) – can be added BACK

- Insurance (line 9) – Added Back

- Mortgage Interest (Line 12) – Added Back

- Taxes (Line 16) – Added Back

And this is why owning property is such a great method of building wealth. Nearly all of your normal expenses on a property can be deducted from your TAXABLE income but added BACK to your qualifying income for a conventional loan!

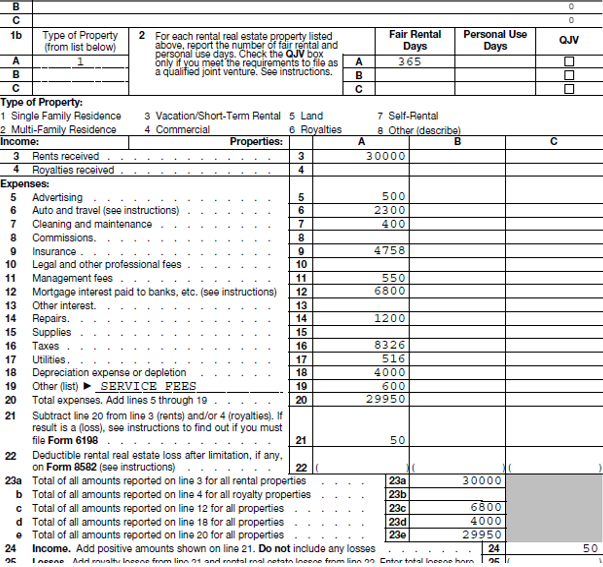

Let’s examine an actual tax return SCHEDULE E below. Don’t worry, all the personal information has been removed.

Line 3 is all the income that was made – $30,000! Wow!

But examine line 21 – $50 in taxable income…great job! But will this scare a lender? Not if you are claiming your deductions correctly. This person claimed $4,758 in insurance (Line 9), $6800 in mortgage interest (Line 12), $1200 in repairs (Line 14), $8326 in taxes (Line 16), and $4000 in depreciation (Line 18)….for a total of $25,084. So a taxable income of $50…but a qualifying income of $25,084! Now this is held against the expense that you have on the property (mortgage, etc) but claiming your deductions is a MUST for Fannie/Freddie loans. This subject can be explored at length but for the sake of time let’s cover 2 things here quickly:

- LINE 6 – Auto & Travel

Remember above on Schedule C? If this person would claim this auto expense as mileage on Schedule C then his qualifying income would be EVEN BETTER! Keep that in mind – business mileage on Schedule C, Line 44A for Fannie Mae!

- NOT REPORTING.

Now I have seen many a person not claim their deductions on their returns. The most common item I see is when they may have purchased it at the end of the year, and didn’t have any income. YOU SHOULD STILL CLAIM YOUR DEDUCTIONS! Remember, you are not penalized on your loan to claim taxes, insurance, ONE TIME RENOVATION REPAIRS, mortgage interest, and Depreciation! CLAIM THOSE ALL DAY EVERY DAY!

But some of us file other things on Schedule E – Like Corporate Tax Returns or Partnerships. Those get reported here as well. And just like with the others above there are some good deductions you should be taking advantage of here as well.

S-Corp

- W2 income – that’s easy, you probably understood that your W2 income can be added BACK

- K-1 income (box 1 & 2) – also pretty self-explanatory, but just in case, it’s added BACK

- Amortization/Casualty Loss – Added BACK

- Depreciation 1120s (line 14 & 15) – Added Back

However….

- Mortgage Notes, bonds payable in less than 1 year (Schedule L, line 17)- this is SUBTRACTED from your income

- Meals & Entertainment (Schedule M1, Line 3b) – SUBTRACTED from your income

- Non re-occurring Other Income (1120s line 5) – SUBTRACTED from your income

Partnerships

- W2, K1 (box 1,2, & 4), Depreciation, Amortization/Casualty Loss – all added BACK

- Non re-occurring Other Income, Meals and Entertainment, Mortgage Notes payable in less than 1 year, AND Ordinary income from Other (1065 line 4) – all SUBTRACTED from your income

What a lot of information and we could probably spend ENDLESS amounts of time on this subject. But this post was designed to help highlight what you should be targeting to help you qualify for Fannie/Freddie (Conforming, Conventional) residential loans on 1-4 unit properties.

*Andrew Postell is a former Marine, an Investor, and a lender. He specializes in Texas and lending on investment properties. For more information, go to www.rate.com/andrewpostell

Recent Comments